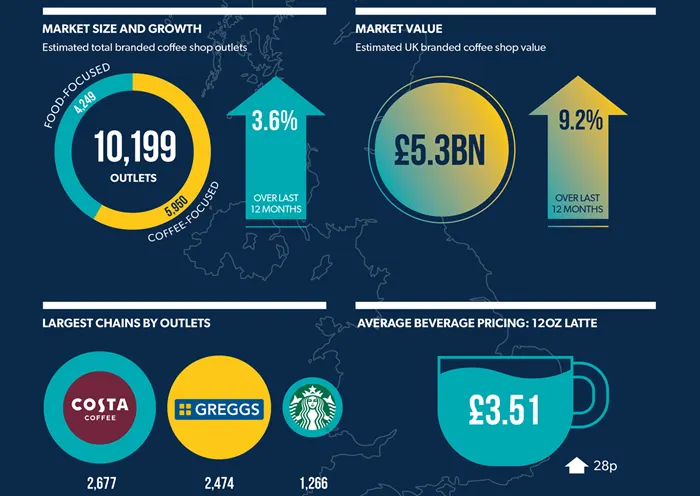

Project Café UK 2024 shows the £5.3bn UK branded coffee shop market achieved 9.2% sales growth over the last 12 months, expanding 3.6% to reach 10,199 outlets. While total sales are above pre-pandemic levels, weakened consumer confidence, high inflation and lower footfall at traditional prime locations have contributed to slowed growth and increased uncertainty

- UK branded coffee shop market achieved 9.2% sales growth to reach £5.3bn over the last 12 months

- Total market grew 3.6% by outlets to reach 10,199 stores

- Outlet growth led by Greggs and Starbucks, which opened 73% of all net new stores

- Average price of a 12oz latte rose 8.7% to reach £3.51

- 25% of branded coffee business saw net reductions in their outlet portfolios

Outlet growth slows as operators exercise caution

The enduring appeal of coffee shop culture in the UK has enabled the market to weather weakened consumer confidence, high inflation and growing competition over the last 12 months.

Indicating that operators are increasingly assessing underperforming sites, a quarter saw net reductions in their outlet portfolios over the last 12 months, with 29% not opening any net new outlets amid heightened industry caution. However, highlighting the easing of inflationary pressures over the last 12 months, the proportion of industry leaders describing trading conditions as ‘positive’ rose 12% to reach 49%.

Costa Coffee remains the UK’s largest branded coffee chain, holding a 26% share of the market with 2,677 stores, having closed net 17 sites over the last 12 months. Overall outlet growth was led by Greggs and Starbucks, which opened 73% of the 353 net new stores added to the market during the period.

Coffee’s ‘affordable luxury’ status challenged as UK consumers cut back

The cost-of-living crisis continues to squeeze UK consumer disposable incomes, with World Coffee Portal research identifying a negative impact on regular coffee shop visitation over the last 12 months.

Amid sustained high product, labour, energy and property costs, branded coffee chains have increased coffee prices by an average of around 9% over the last 12 months – leading to a 9% fall in consumer satisfaction with value-for-money. Average spend also fell 4% year-on-year, with consumers either more likely to only purchase a beverage or spend less overall on food items.

Operators deploy new sales channels to stay competitive

In an increasingly competitive UK branded coffee shop market now exceeding 10,000 stores, many operators are diversifying retail and product strategies to broaden their market appeal.

In a bid to attract younger consumers, Costa Coffee became the first major UK branded coffee chain in the UK to offer bubble tea in 2023 and has also launched a new hot milkshake range. Meanwhile, Costa, Starbucks and Tim Hortons all grew their drive-thru presence over the last 12 months to collectively hold a 93% share of the 801-site UK drive-thru coffee market.

In the food-focused segment, Greggs met its target to open circa 150 stores per year with a significant coffee offering and the chain is now trialling iced coffee at selected locations. Meanwhile, Pret A Manger has doubled down on its in-store subscription with a 20% food discount to subscribers and has sought to cater to family trade by introducing a new children’s menu.

Improving economic outlook for 2024 predicted – but growth expected to remain subdued

UK inflation has more than halved over the last 12 months and high street trading conditions are likely to improve further following the Bank of England’s anticipated base rate decrease – its first since March 2020. However, fierce competition in an increasingly crowded market is likely to constrain operator growth.

World Coffee Portal forecasts the total branded coffee shop market will exceed 10,500 outlets by January 2025, and more than 11,600 by January 2029 at five-year outlet growth of 2.7% CAGR. Sales are expected to exceed £7.2bn over the same period, representing five-year growth of 6.2% CAGR.

Commenting on the report, Allegra Group Founder and CEO, Jeffrey Young said: “Despite some very strong economic headwinds, squeezed consumer spend and trading uncertainty, the UK coffee shop market – and especially branded coffee chain segment – has remained very resilient. Having achieved two decades of consistent growth only interrupted by the Covid era, we’re now looking at trading patterns well above pre-pandemic levels.

“A very bright future awaits for the UK coffee shop market as operators invest in innovation through technology, capture the hearts and minds of the next generation with new product categories, including iced beverages, and focus on delivering high-quality, value-for-money experiences.”

{kind=link}